I still remember the view I shared whenever I was asked over the past few months: NVIDIA (NV) at 100-110 is cheap. Now, as the world "seems" to have returned to the state before April 2nd, NV has also stood above 135. While reflecting, it's not about whether the view was correct or not; rather, looking back at this process, the underlying market patterns might be more worth discussing.

The fundamentals are right there: NV still has the world's best computing chips, an unshakeable "CUDA ecosystem," global demand for AI computing power remains strong, technical uncertainties regarding Blackwell clusters still exist, and doubts about the high investment vs. low economic return of AI models persist...

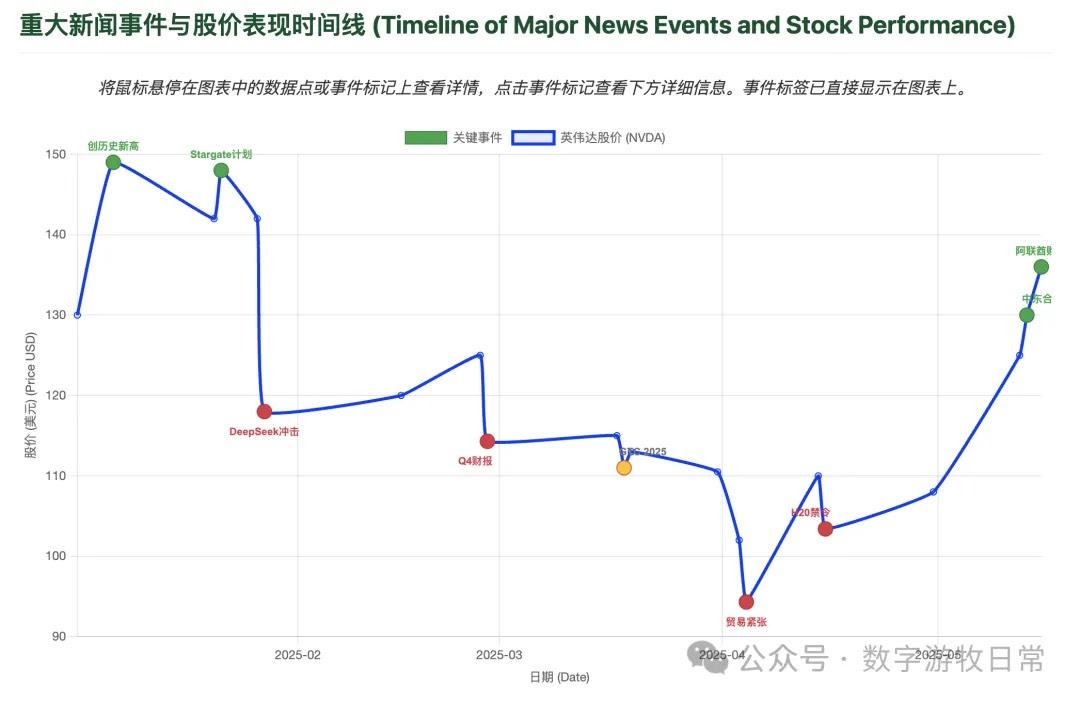

Yet, since the beginning of this year, NV's stock price has carved out a sharp "V-shape."

Each of these fluctuations had traceable signs beforehand and could be understood afterward, but I believe it is very difficult to find a fixed method, routine, or strategy that could extract substantial returns from such large swings exceeding 30% in both directions.

A "buy and hold" strategy wouldn't have worked; even calculating from the start of the year, returns only turned positive by the close of the US market this morning.

Trading based on the belief that a "tariff war" would ease also faces logical challenges. While many placed heavy bets at the bottom during the most panicked days, the window below 100 was actually quite short. Furthermore, if the concern was the tariff shock, then even if they were fully canceled, the logical conclusion would be a return to prices before April 2nd. The profit margin would be small, making it very difficult to capture the subsequent 110-130 rally.

So-called event-based fundamental analysis would hit walls everywhere: "Stargate" was clearly a major positive, DeepSeek looked like a massive negative shock, and Microsoft’s downward revision of data center construction plans was also real...

Everything seems reasonable, but the stock price fluctuated rapidly the moment the events occurred. Any entry or exit point based on analysis after the event meant the market had likely already "digested 60-70% or more" of the news.

Yes, we could think of pure quantitative methods using high-frequency technical indicators. However, from my experience of real-time daily observation, while some patterns exist, any counter-trend sudden fluctuation in the market is larger than the regular patterns. This means the risk of loss is significantly higher.

Of course, I can still insist that "100-110 is cheap," but the struggle NV faced over the past quarter was real. If the earnings report on May 28th reflects the substantive impact of these "struggles," then that conclusion would need revision. The problem is, the market may not grant the opportunity for revision and re-adjustment of trades.

Indeed, these discussions—which border on "sophistry"—apply not just to NVIDIA; it’s just a typical example of an asset I thought I had researched deeply.

Using this as an example, "investment" and "research" are rapidly decoupling.

This decoupling has always been happening. Recently, as more people focus on and review consumption, they use examples like Pop Mart, Lao Pu Gold, Ruoyuchen, or even the pet economy. They conclude that it is precisely through tracking data and long-term deep research that one can "discover value."

I’m sorry, but if you take the successful experience of individual cases, summarize them into quantifiable indicators, and then perform "systematic backtesting" across more assets, the results are basically "disastrous." Such results don't mean that no one can succeed consistently; they simply signify "lack of reproducibility."

This is a point where "quant" often challenges "active" management. But conversely, as multi-factor models become "crowded" into high-frequency price-volume data and occasionally encounter the "liquidity traps" of small-cap stocks, the myths have either been shattered or are on their way to being so.

Perhaps, the result of modeling structured and unstructured data with a "God’s eye view" only points to one "metaphysical factor": conviction.

Believing in NVIDIA is a conviction; believing in Apple is a conviction; believing in Moutai is a conviction; believing in Coca-Cola is a conviction...

Behind conviction, one can certainly find many deep, non-reproducible reasons. But to this day, no one has been able to replicate Warren Buffett, have they?

Talking about these things isn't always happy, so let's do something happy. For example, let's see how much models have progressed and what new things we can play with right now.

For instance, when I considered doing a review of NV’s performance this year, I definitely didn't do it myself. I handed it over to Deep Research, Claude, and Gemini.

Although many people, including myself, noticed more and more bugs after Gemini-2.5 released its May 6th update—even complaining that the "model might have broken itself"—the results generated in one go today were surprisingly satisfying:

Of course, the content is all thanks to OpenAI's Deep Research.

In contrast, under the same prompt, the results from Claude 3.7 weren't necessarily bad; they just didn't look as professional or focused as Gemini-2.5. There was also a major error: Intel's stock price was wrong.

I really like this final insight from Deep Research: Sentiment can more often be used as a contrarian indicator, and stock price turmoil stems from "narrative changes" rather than fundamental changes.

Immersing myself in working with AI has always brought me more joy. As an old quantitative researcher and programmer who increasingly uses active research frameworks and methods, I have become more skeptical of the systematic (reproducible) integration of quantitative methods.

However, the happiness derived from the technical level remains pure, joyful, and sustainable.

I increasingly feel that this is a way to generate a stronger "sense of conviction." I am who I am, and thus, it is time to let go of the obsession with "reproducibility."