Market Depth Research Daily (2025-07-16): Market Divergence Under Tariffs and Technology Waves

After a period of accumulation, experimentation, and solidification (most importantly, refocusing on my core expertise: Market and AI after a brief hiatus), I am launching a new daily update series: Market Depth Research Daily. 1. Focused exclusively on overseas markets; 2. In-depth analysis of the daily's most impactful factors; 3. Entirely powered by AI. This is the first edition.

Core Summary

On July 15, 2025, the US stock market exhibited a significant and deepening bipolar pattern. The tech-heavy Nasdaq 100 Index (QQQ) remained resilient, supported by long-term growth trends in Artificial Intelligence (AI). In sharp contrast, the Dow Jones Industrial Average (DIA), dominated by industrial stocks, plummeted due to escalating trade and tariff concerns.

Behind this divergence are two major and opposing forces. First, aggressive and unpredictable US trade policy—characterized by broad-based tariffs and a looming August 1 deadline—has created significant headwinds for cyclical sectors, dampening investor sentiment and leading to cautious corporate guidance. Second, the ongoing massive capital investment cycle in AI infrastructure provides a resilient, non-cyclical growth narrative that allows key tech leaders to remain insulated from broader macro volatility.

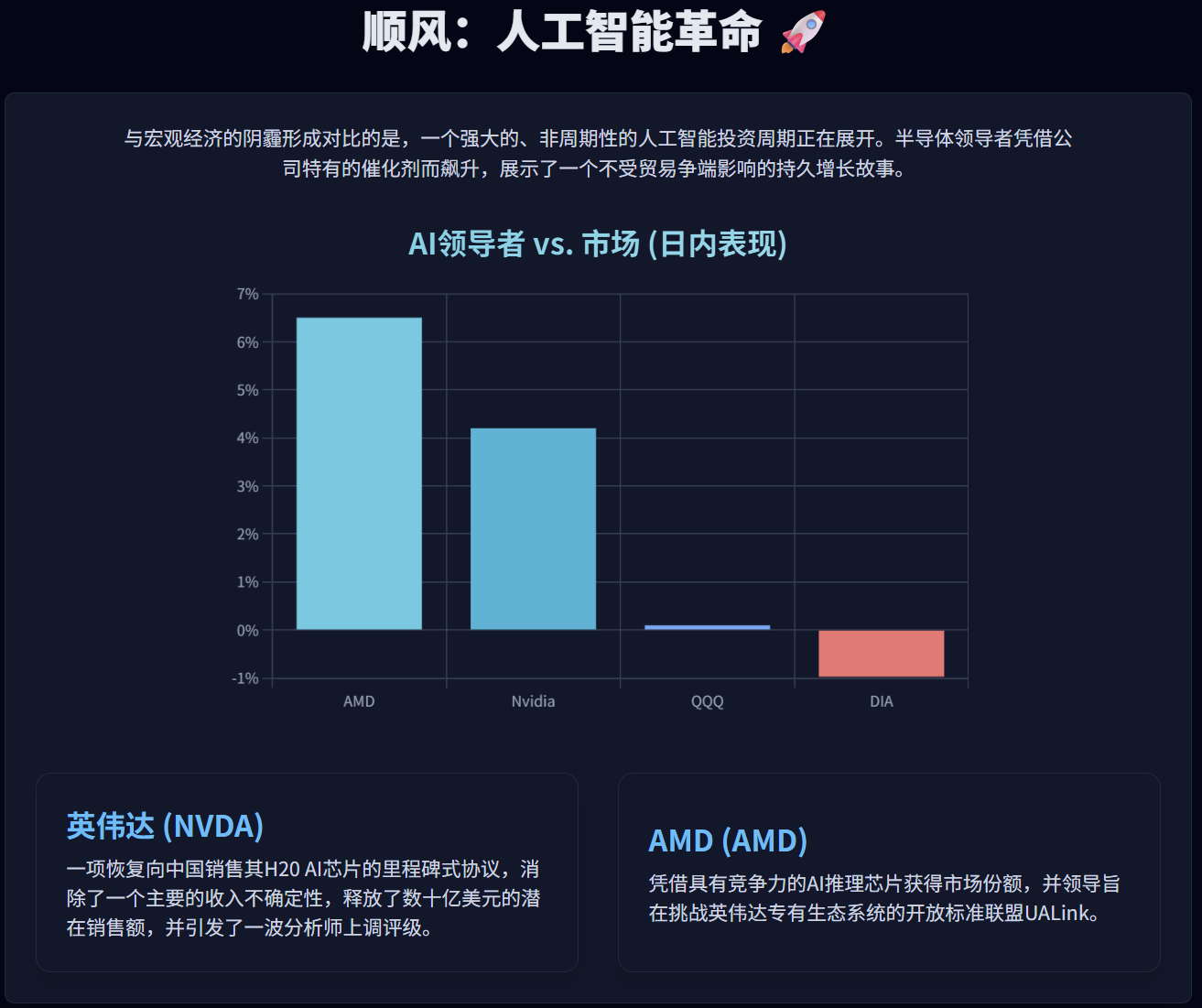

The day's market movement perfectly illustrated this split: top performers included AI chipmakers Nvidia and AMD, as well as strategic domestic leaders benefiting from "onshoring" and national security tailwinds, such as MP Materials and Steris. Conversely, laggards were concentrated in sectors most sensitive to economic cycles and trade policy risks: banks (like JPMorgan Chase) and industrial metal mining companies.

At the heart of the current market landscape is the conflict between cyclical fears and secular growth. While short-term volatility will be dictated by the August 1 tariff deadline and the Federal Reserve's response, underlying structural trends like AI adoption and strategic supply chain restructuring are creating unique long-term investment narratives. This environment favors a selective, theme-driven investment approach over broad market exposure, rewarding investors who can distinguish cyclical noise from secular signals.

Part I: The Macro Pressure Cooker — Analyzing the 2025 Tariff System

1.1 Architecture and Economic Consequences of the Trade War

Widespread market anxiety stems from a complex and evolving US tariff system. It is characterized by broad-based and escalating tariffs targeting major trading partners, creating a highly uncertain environment for global commerce. A critical turning point is the upcoming August 1, 2025 deadline, which has become the focal point for the market.

Key tariff measures include:

- A 20% broad tariff on Chinese imports.

- A 30% tariff on all Mexican imports.

- Announcement of new 30% tariffs on the EU and Mexico effective August 1.

- Abolishment of the "de minimis" exemption for Chinese imports, making all goods subject to duties.

- Heavy tariffs on steel and aluminum.

According to quantitative analysis by the Yale Budget Lab (TBL), these tariffs represent a measurable drag on the US economy:

- Household Costs: Resulting in an average effective tariff rate of 20.6%, costing the average US household approximately $2,800 in 2025.

- GDP & Employment: Projected to reduce US real GDP growth by 0.9 percentage points in 2025 and result in the loss of 641,000 jobs.

- Sector Impact: While manufacturing output is expected to grow by 2.6%, this is offset by contractions in construction (-4.1%) and agriculture (-0.8%).

1.2 Ripple Effects: Bond Yields, Inflation, and the Fed's Dilemma

Tariffs are pushing up inflation (June CPI reached 2.7%) while threatening economic growth. This keeps long-term Treasury yields elevated due to fiscal risk concerns, even as the market expects the Fed to cut rates in response to a slowing economy. This disconnect puts immense pressure on banks that rely on a stable yield curve. Consequently, the Fed is caught in a dilemma: needing to cut rates to support the economy while simultaneously needing to curb tariff-driven inflation. The July 30 Fed meeting will be a critical moment for the market.

Part II: A Tale of Two Markets — The Great Divergence of 2025

2.1 Industrial Malaise in the Dow vs. Tech Resilience in the Nasdaq

The Dow Jones (DIA) fell due to its constituents' (e.g., Caterpillar, JPMorgan) high exposure to global trade risks. Conversely, the Nasdaq (QQQ) rose because the business models of tech and growth companies are perceived as more resilient to physical commodity trade conflicts and benefit from powerful secular trends like AI. The market is voting with capital, favoring the durable growth of tech stocks over the uncertainty of cyclical sectors.

2.2 "Magnificent" Leaders vs. the Laggards

Market leadership is extremely narrow, with the health of the S&P 500 heavily dependent on a few tech giants (the "Magnificent Seven"). These companies contributed nearly half of the first-quarter earnings growth, and their massive Capex plans serve as a vital engine for economic activity. Meanwhile, the Russell 2000, representing small-cap stocks, continues to decline, as these smaller firms are more vulnerable to tariffs and inflation due to a lack of pricing power.

Part III: Leaders of the New Economy — Analyzing Outperforming Stocks

3.1 The AI Arms Race: Nvidia and AMD

Nvidia (NVDA): Shares hit record highs, with the primary catalyst being the approval to resume sales of its H20 AI chips to China. This move eliminated a major financial uncertainty, leading Wall Street analysts to significantly raise price targets, believing a full recovery in China sales will greatly drive future revenue growth.

AMD: Shares also surged, benefiting from its strong competitive position in AI inference and its leadership in the UALink consortium. The consortium aims to develop an open-standard AI accelerator interconnect technology to challenge Nvidia's proprietary NVLink ecosystem, offering significant growth potential for AMD.

3.2 Securing Domestic Supply Chains: MP Materials (MP) and Steris (STE)

MP Materials (MP): The rare earth producer's stock soared on two transformative deals. First, a landmark public-private partnership with the Department of Defense (DoD), including billions in commitments and direct equity investment. Second, a $500 million long-term supply agreement with Apple. These deals establish MP as a central player in rebuilding a complete rare earth supply chain in the US, making it an effective tool to hedge against escalating US-China trade tensions.

Steris (STE): As a global leader in infection prevention, Steris embodies the appeal of "defensive growth." Its business is tied to relatively non-cyclical global surgical volumes while benefiting from the trend of onshoring medical devices and holding long-term contracts with the DoD. Solid financial performance and strong guidance make it an ideal choice for investors seeking growth with a margin of safety.

Part IV: Laggards and Headwinds — Deconstructing Underperforming Sectors

4.1 The Banking Struggle

Despite major US banks (like JPMorgan Chase and Wells Fargo) reporting second-quarter profits that exceeded expectations, their share prices lagged. This is because bank executives issued extremely cautious outlooks, explicitly pointing to risks from tariffs, trade uncertainty, and an unpredictable yield curve. Wells Fargo lowered its full-year Net Interest Income (NII) guidance, directly blaming the impact of tariffs on client borrowing, which particularly unsettled investors.

4.2 The Mining Conundrum

The mining and materials sector serves as a direct barometer of global macroeconomic health. With expectations for global economic growth lowered due to the trade war, producers of industrial metals like copper and aluminum are facing the dual pressure of weakening demand and rising input costs. However, there is divergence within the industry: gold miners are experiencing a "financial renaissance" as geopolitical and trade uncertainty push gold prices to record levels, making them a direct tool to hedge against market instability.

Part V: Outlook and Strategic Recommendations

5.1 Upcoming Catalysts

Key events in the coming weeks will determine the market's direction:

- August 1: Deadline for new tariffs on the EU, Mexico, and others to take effect.

- July 29-30: Federal Reserve FOMC meeting, which will reveal the path of monetary policy.

- August 5 and 27: AMD and Nvidia will report earnings, respectively, serving as critical tests for the AI growth narrative.

5.2 Investment Strategy Advice

Continue to Overweight Secular Growth Themes: Maintain overweight positions in AI hardware leaders (Nvidia, AMD) and strategic domestic champions (MP Materials, Steris). Growth in these companies is driven by structural shifts rather than short-term cycles. Remain Cautious on Cyclical and Interest-Rate Sensitive Sectors: Until trade and monetary policies become clearer, the risk/reward profile for industrials, materials, and financials remains poor; a neutral or underweight stance is recommended. Favor Quality and Defensive Characteristics: In a volatile market, focus on companies with strong balance sheets and abundant free cash flow. Consider including assets like gold miners in portfolios to hedge against geopolitical risk.

Final Conclusion: The current market requires a refined strategy capable of identifying profound divergences. Portfolios should be positioned to capture the secular growth of technology and strategic domestic industries while hedging against macroeconomic risks brought by unpredictable trade policies.

If visualized, the effect is as follows (we can see at least one "illusion" regarding the market performance of DIA and QQQ; the research article does not actually track performance since April, so the visualization is likely intended to "vividly" demonstrate the divergence):