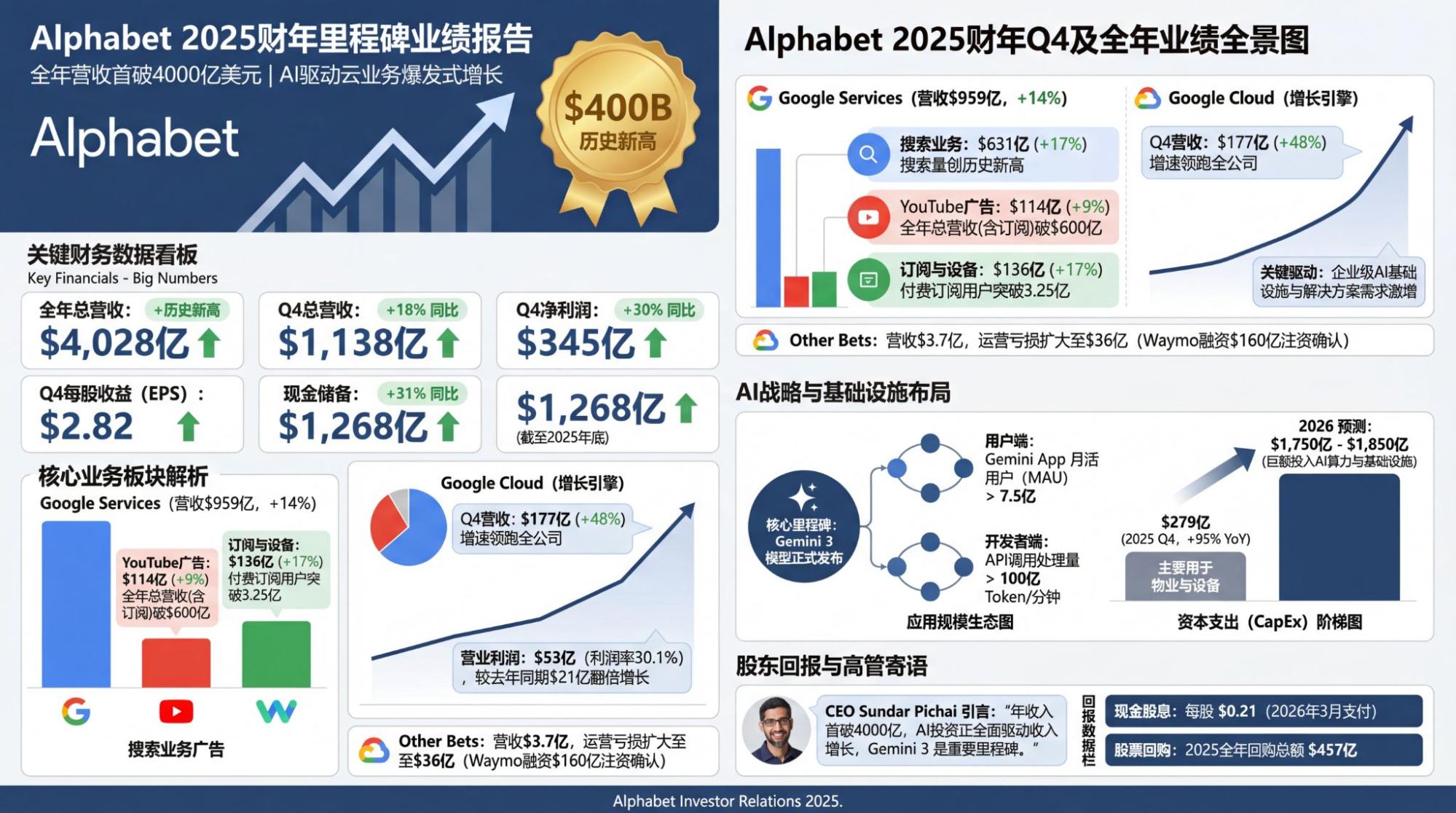

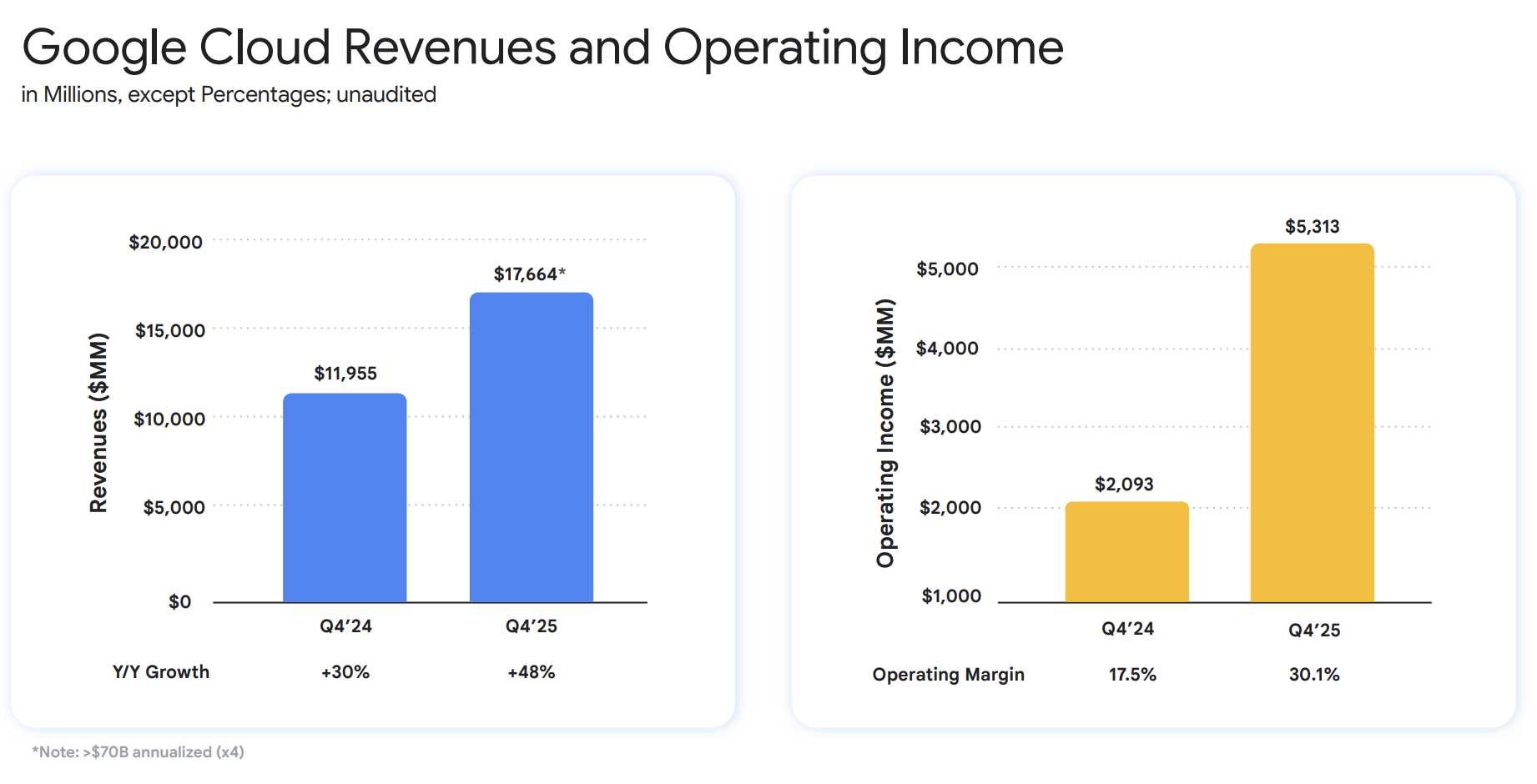

Google does not disappoint. Although my previous forecast was relatively conservative—simply calculating that cloud revenue growth would cross the 40% threshold and gross margin would increase by one or two percentage points to leave room for upside—the results were even better.

The actual performance was a pleasant surprise, allowing me to continue my blatant favoritism: Cloud growth at 48%, with gross margins exceeding 30%. As I said over two years ago, Google Cloud is the only one capable of continuously increasing gross margins through AI, because it has an immense potential to convert free users to paid ones. Developers are willing to pay for Gemini; they have in the past, and they will even more in the future.

I have also always maintained that generative AI lacks user stickiness, except for Gemini.

The market should have responded very positively to these results, unless...

The "unless" is the even larger-than-expected capital expenditure (Capex) plan: $185 billion to $195 billion for the full year of 2026. If this figure is realized, it would be nearly double that of 2025. Consequently, the market hesitated (as soon as the earnings report was released, the stock dropped upon seeing the Capex, then stabilized after reviewing the revenue details).

The market simply does not like excessive Capex anymore.

However, looking at it calmly: first, past investments have clearly driven significant growth; second, setting a plan is one thing, but execution is another. Management is clearly aware of the market's concerns and has offered buybacks as a hedge.

Still, my view remains unchanged: while every company will provide high Capex guidance, given the various physical constraints currently observed, a large question mark remains over how much of that can actually be executed.