Thanks to NotebookLM, I've discovered some overlooked details in the Earnings Call.

Regarding the impact of capital expenditure (Capex) and storage prices, these were just two brief sentences in the transcript. I didn't notice them while reading on my phone, as my attention was diverted to how much computing power the $37.5 billion quarterly Capex roughly corresponds to. It was only after processing it with NotebookLM that I saw the information in the screenshot above. After further inquiry, the situation appears to be as follows:

Of course, Microsoft did not provide further explanation. Combining this with some of my previous views and making some adjustments, the status might look like this:

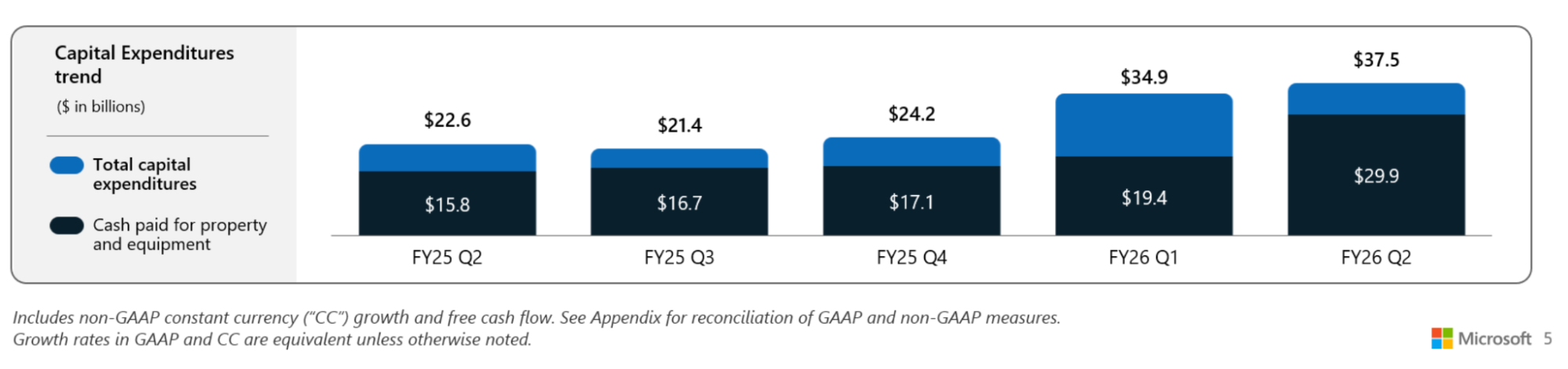

- Although Capex grew by $2.6 billion quarter-on-quarter (QoQ) this quarter, the structure has changed significantly, returning to the previous state where nearly 2/3 is allocated to short-life equipment (primarily GPUs and CPUs).

- In FY26 Q1 (the previous quarter), the proportion of long-life assets was significantly higher. This likely explains why data center capacity increased by nearly 1GW in the fourth calendar quarter of 2025 (it wasn't specified if this includes leased capacity like Nebius).

- Looking at the volume of spending on long-life assets, the quarterly addition of data center capacity in the first half of calendar year 2026 should be lower than that of Q4 2025.

- Management explained the QoQ decrease in Capex (while maintaining a stable structure) as fluctuations in the normal construction cycle of cloud infrastructure. From the overall context, while this is a fact, a large reason for this framing is likely to appease the market.

- Another reason should be preparations for the transition from Blackwell to Rubin.

- This can basically be seen as the initial signal of big tech companies starting to scrutinize Capex plans, a point I repeatedly emphasized in offline discussions late last year.

- Furthermore, Microsoft's explanation of revenue growth is quite clear: if they leased out more compute, cloud business revenue growth could exceed 40%. However, they must reserve compute for enterprise and individual customers (various Copilots). This further demonstrates that the ROI performance of model services is lower than that of the overall cloud business.

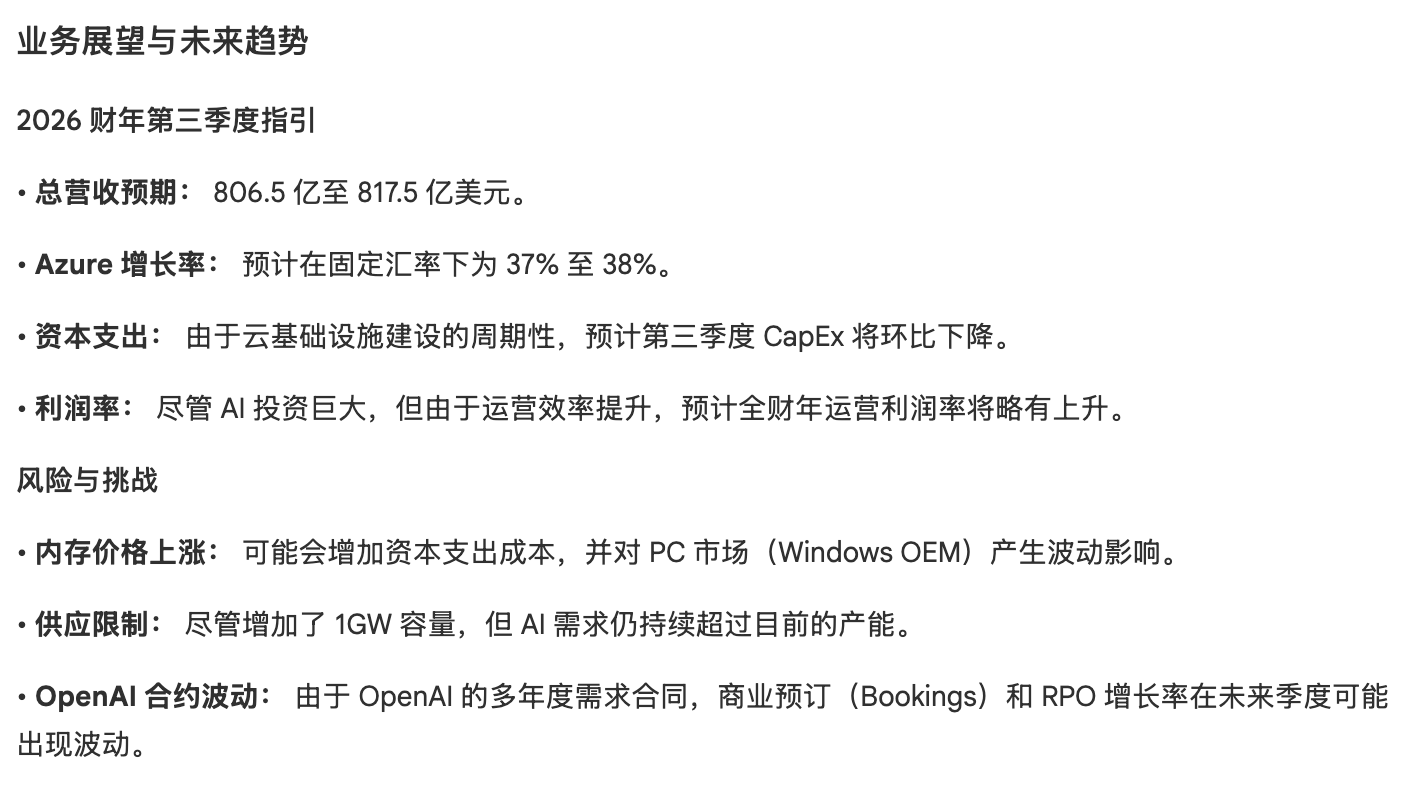

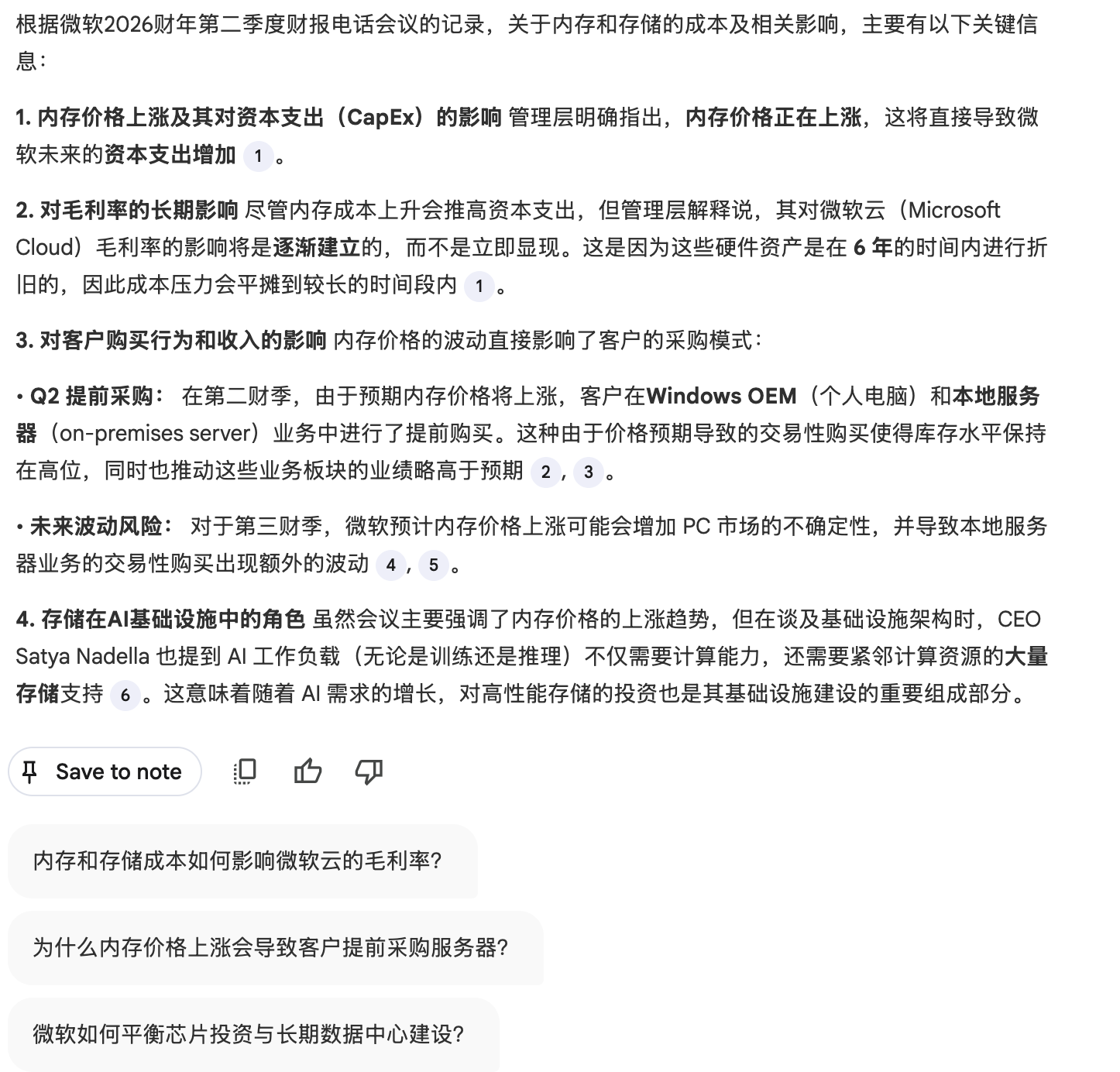

- Returning to memory and storage, it is clear that Microsoft's statements are starting to hint that negative feedback caused by price increases has already begun: many users placed orders early, so related business slightly exceeded expectations this quarter, but it might be relatively weaker in the future.

- Meanwhile, due to rising storage prices, Microsoft expects Capex to rise as well. Although the financial impact will be smoothed out over the next 6+ years on a quarterly basis, this will likely further reduce ROI.

- As an additional point: although everyone says model costs will become cheaper, and although I previously predicted model prices would drop by 2/3 in 2026, substantial price cuts have not yet happened. Take Gemini as an example: early last year, the input/output pricing for 2.5-flash was $0.3/$2.5 respectively; today, Gemini-3-flash is $0.5/$3. Currently, price is clearly the most important factor affecting demand and implementation. As storage prices account for an increasingly high proportion of compute costs now and in the future, we need to watch out for a series of negative feedback chain reactions.

- Those who know me know that my style in trend judgment tends toward caution. My view that "memory bandwidth and capacity determine computing power" has remained unchanged for over three years. However, problems that the outside world might not have deeply recognized in past years have now likely manifested by 80-90%. Also, this post serves as a small test: I've noticed that WeChat Channels/Official Accounts have made significant adjustments in information push algorithms, and traffic has changed noticeably.