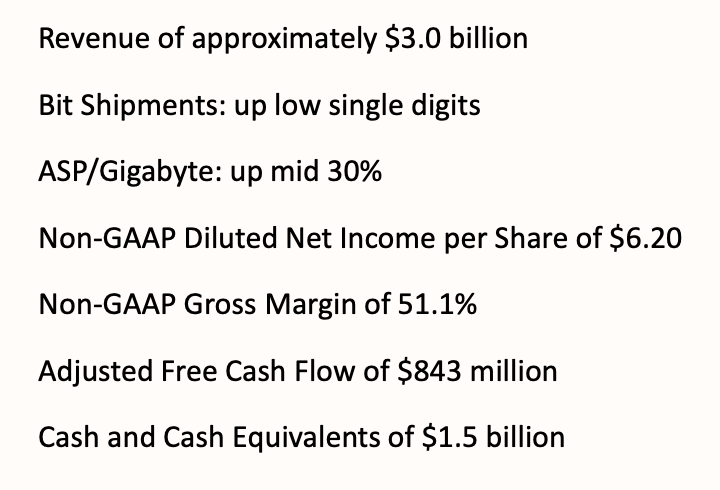

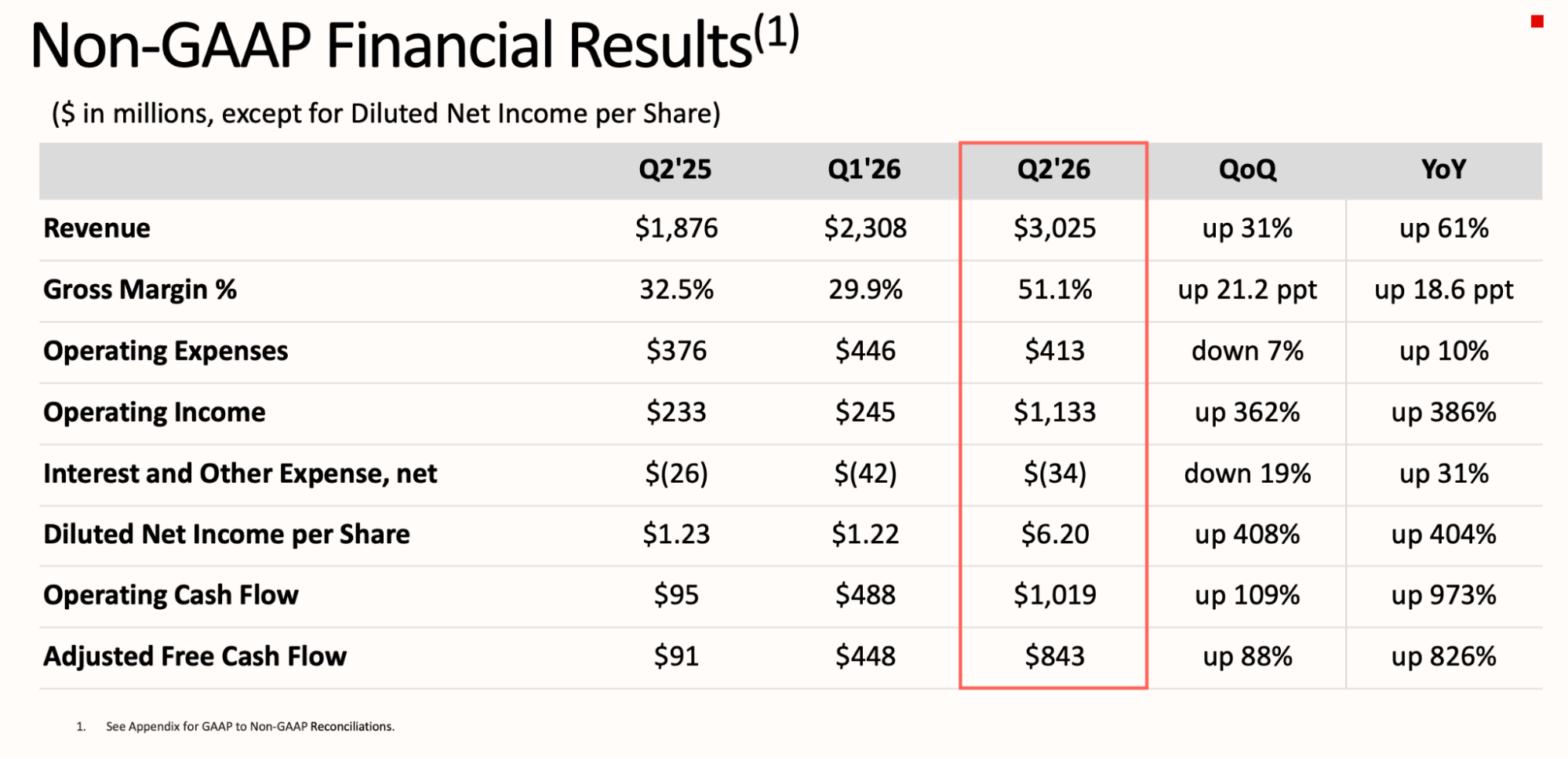

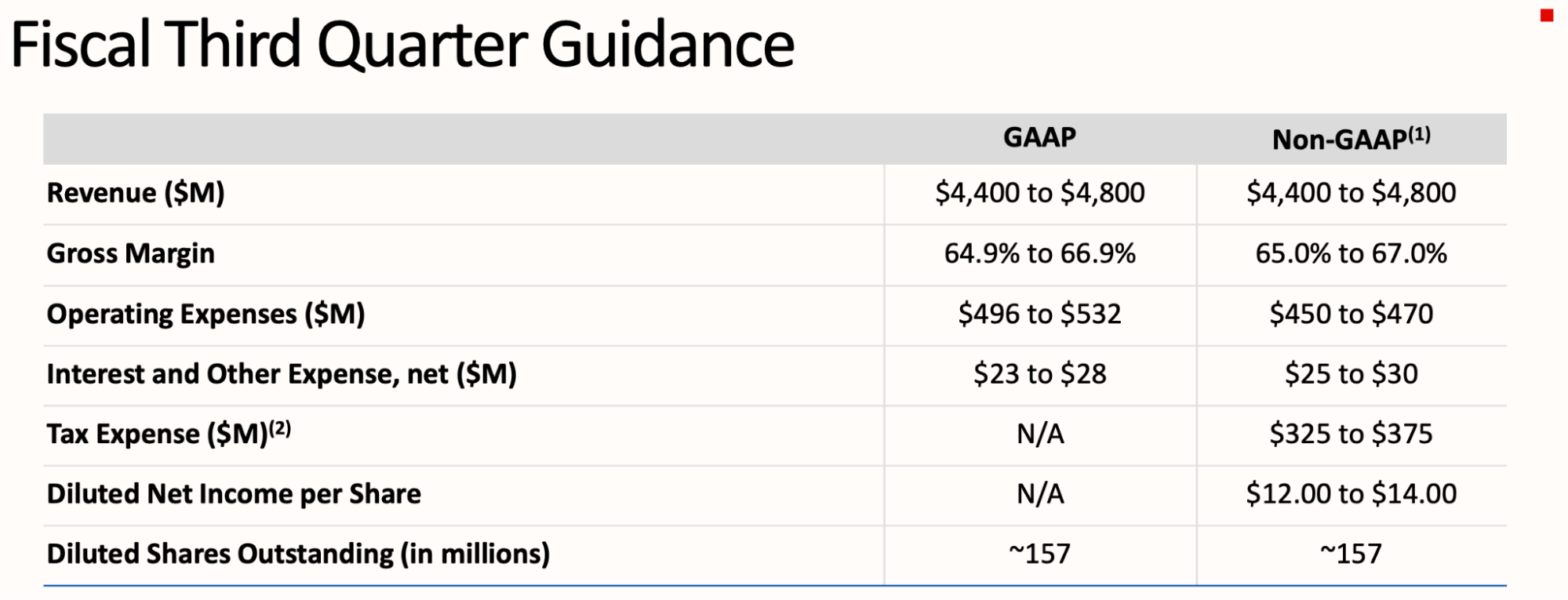

SanDisk's earnings report was "significantly better than expected" as anticipated, and the outlook for the next quarter is also "explosive"; there is almost no doubt about the super cycle.

The only flaw might come from: "Bit Shipments" showed only single-digit growth. In other words, sales volume measured by capacity grew by single digits, and revenue was driven entirely by "price increases."

Profit goes without saying, with gross margins rising significantly.

Next quarter's outlook is also extremely optimistic, with momentum still building.

Here are some points I think are worth mentioning in the article:

In the short term, SSDs have more explosive power than Memory. However, over the long term, Memory will be much healthier. In fact, Memory has a chance to break its cyclicality, or at least significantly extend the boom cycle. The SSD super cycle is still a cycle; low growth in delivered capacity can be interpreted as "shortage" in optimistic times, but in pessimistic times, it means there is no room for growth.

Will the current shortage in storage affect the deployment pace of data centers? It's possible, but the constraints being observed are more related to data center infrastructure (land, power, power supply equipment, etc.).

How much more price increase can the end-users (mainly chips, servers, and CSPs) tolerate? Due to competition, tolerance is certainly higher than in past cycles. However, as this extends through the industry chain to the final AI users (token consumers), someone will eventually see their gross margin decline by "absorbing" these costs. Microsoft is already showing signs of this, but I don't believe CSPs will be the "hardest hit," as they have massive scale and room to "optimize user experience" and digest unfavorable factors.

As I wrote in yesterday's article, I believe Microsoft's tone indicates they are already seriously responding to this. Although the signal is very early, "negative feedback" may have already begun.

Of course, as I noted yesterday, I have always had a low risk preference. Objectively speaking, the cycle is certainly not over, but the uncertainty brought by pure price games is increasing significantly. If we believe in the $500 billion or $1 trillion pie painted by NVIDIA, then what we are seeing now is a game of dividing that pie.

It’s clear that WeChat official accounts have changed their rules. Many people likely missed yesterday evening’s article. Since I think it was well-written, I am posting it again as a test.

I’m also attaching a visualization from NotebookLM.

Thanks to NotebookLM for helping me discover some details in the earnings call that I hadn't noticed.

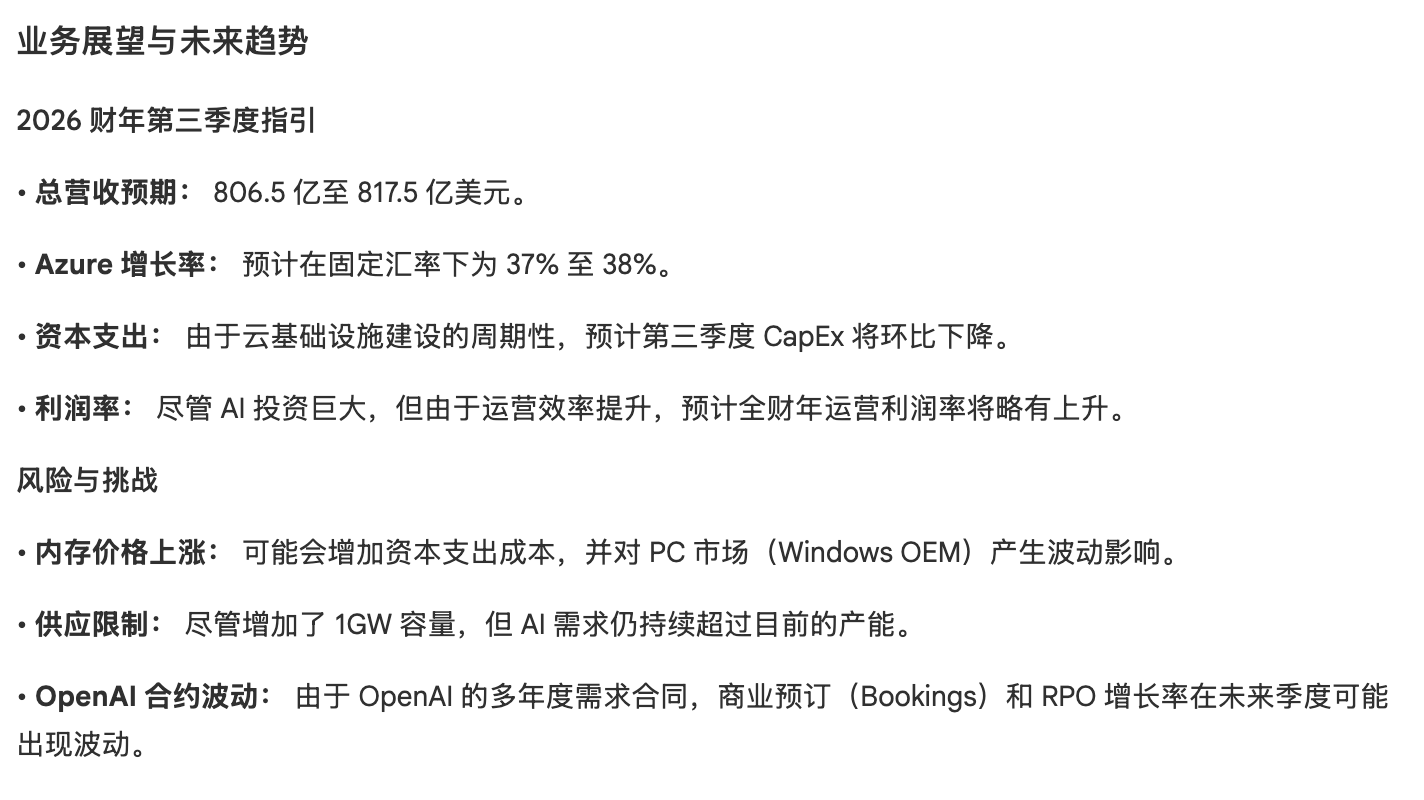

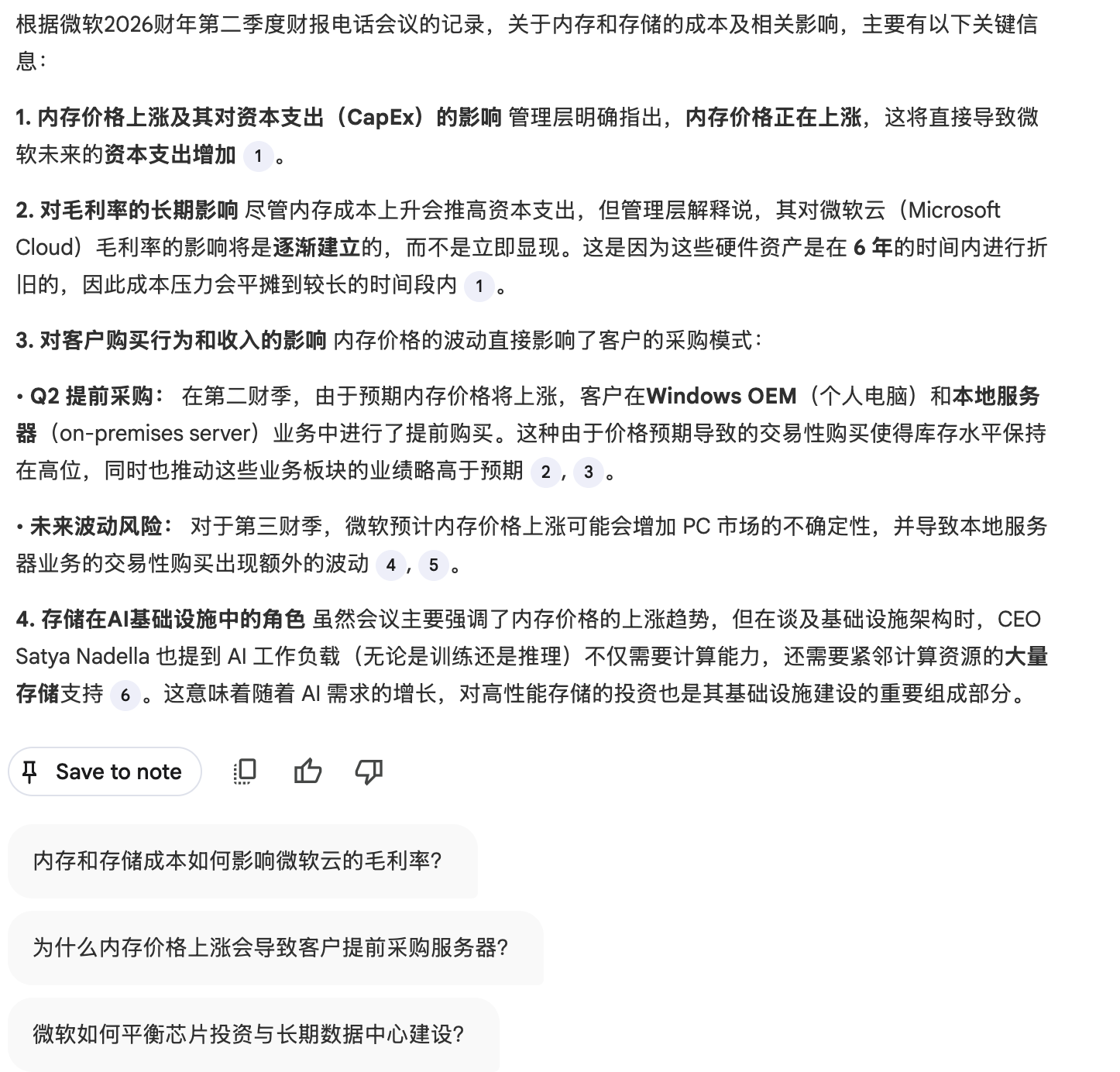

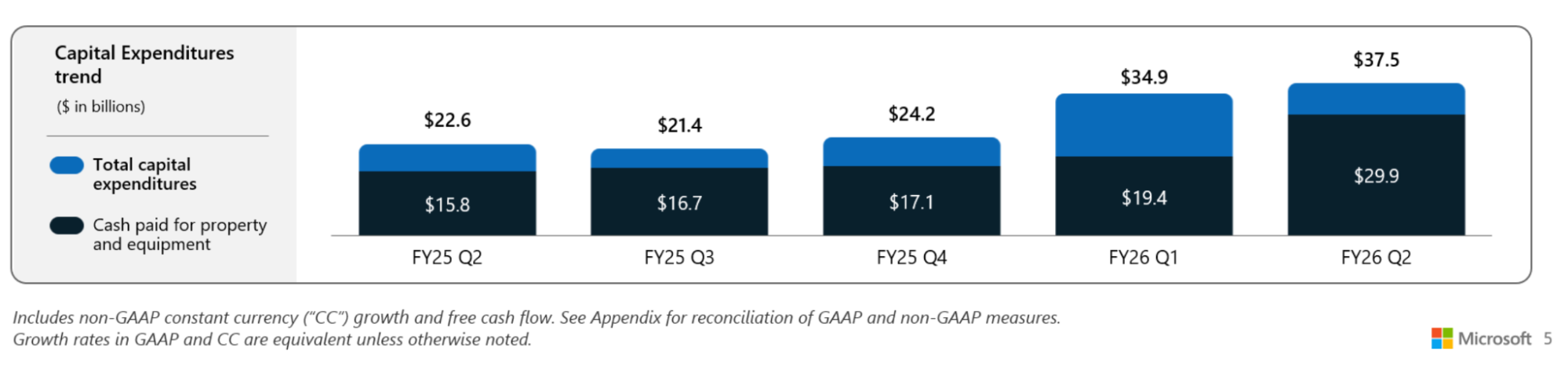

Regarding capital expenditure and the impact of storage prices, these were just two brief sentences in the transcript. I didn't notice them when reading on my phone, as my attention was diverted to how much computing power the $37.5 billion quarterly Capex corresponded to. After processing with NotebookLM, I saw the information in the screenshot above. Upon further inquiry, the situation is roughly as follows:

Of course, Microsoft did not provide further explanation. Combining my previous views with some adjustments, the status might look like this:

- Although this quarter's capital expenditure increased by $2.6B quarter-on-quarter, the structure has changed dramatically, returning to roughly 2/3 allocated to short-lifecycle equipment (mainly GPUs and CPUs);

FY26 Q1 (the previous quarter) had a significantly higher proportion of long-lifecycle assets. This likely explains why data center capacity increased by nearly 1GW in Q4 of calendar year 2025 (it wasn't stated if this includes leased capacity like Nebius);

Based on the volume of long-lifecycle asset spending, the new data center capacity in the first half of calendar 2026 on a quarterly basis will likely be lower than in 25Q4;

Management explained the quarter-on-quarter decline in Capex (while the structure remains stable) as a result of normal fluctuations in the cloud infrastructure construction cycle. From the overall context, while this is true, a large part of it is intended to reassure the market;

Another reason is likely preparation for the transition from Blackwell to Rubin architecture;

This can basically be seen as the preliminary signal of major players beginning to scrutinize their capital expenditure plans, something I repeatedly mentioned in offline exchanges late last year;

Additionally, Microsoft's explanation regarding revenue growth is clear: if they leased out more computing power, cloud revenue growth could exceed 40%, but they must reserve capacity for enterprise and individual customers (various Copilots). This further demonstrates that the ROI for model services is lower than for the overall cloud business;

Returning to memory and storage, it is evident that Microsoft's statements are starting to hint that negative feedback from price hikes has begun: many users placed orders early, making this quarter's business slightly exceed expectations, but future performance may be relatively weaker;

Meanwhile, due to storage price increases, Microsoft expects Capex to rise. Although the financial impact will be smoothed out over the next 6+ years on a quarterly basis, this will likely further reduce ROI;

As an additional point, although everyone says model costs will become cheaper—and my previous expectation was for model prices to drop by 2/3 by 2026—substantive price cuts haven't happened yet. Taking Gemini as an example, the input/output pricing for 1.5-flash early last year was $0.3/$1.25, while current Gemini-2.0-flash pricing is $0.1/$0.4 (Note: prices vary by version; the original text cites Gemini-3-flash which is likely hypothetical or refers to upcoming models). Currently, price is clearly the most important factor affecting demand and implementation. With storage prices taking up an increasing share of compute costs, we need to watch for a chain of negative feedback loops;

Those who know me know that my style in trend judgment leans toward caution. My view that "memory bandwidth and capacity determine computing power" hasn't changed in over three years. However, the issues the outside world failed to deeply recognize over the past few years have now likely manifested by 80-90%.