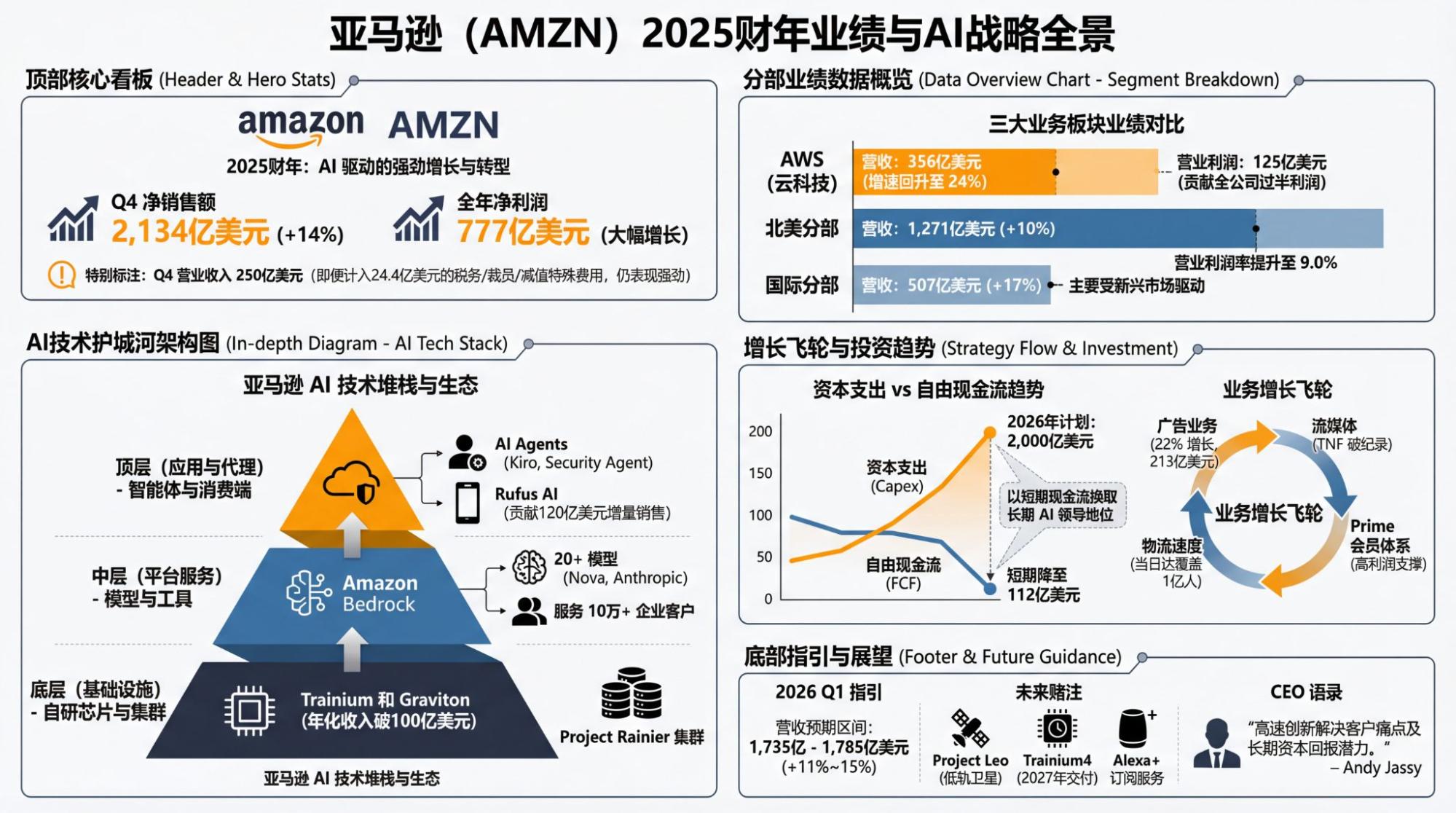

To be honest, I haven't been following Amazon very closely, so I only have a general understanding of market expectations. However, before this earnings report, the one number most people probably cared about was: exactly how much capital expenditure will there be in 2026.

$200 billion—another figure that exceeded expectations. Although it represents less than a 50% increase compared to the actual figures in 2025, the problem is quite simple: Amazon is "running out of money." Free cash flow has dropped quarterly from $38 billion in Q4 2024 to $11.2 billion. If they were to execute $200 billion in capital expenditure, it's very likely that free cash flow for at least some quarters would turn negative. For this company's narrative, that would be very difficult for the market to accept.

However, everyone knows that Amazon has no choice but to follow suit and "place its bets." Otherwise, it wouldn't just be leaving the AI table; the more likely outcome would be AWS falling from its absolute dominance in the cloud. Simply put, AWS's quarterly revenue exceeded $35 billion with a growth rate of 24%. Although the accounting methods differ, Microsoft Azure's figures were $32.9 billion and 28%, while Google Cloud's were $17.7 billion and 48%. AWS is trying hard, but the trend of its market share being eroded is becoming increasingly certain.

It has a lot of catching up to do and many ambitions, including a rumored large stake in OpenAI's new funding round, as well as robotics and aerospace.

In comparison, the slightly better-than-expected revenue and lower-than-expected profit levels seem less significant.

It is a giant still struggling in pain; that's probably the only way to put it.

With the conclusion of Amazon's earnings, the climax of the first round of financial reporting is nearly over. Next, we look toward Nvidia around the end of the month, as well as AVGO, MU, and others. Of course, Oracle will also be a very important object of observation, though it will certainly be very "stubborn" (refusing to admit weakness).

Indeed, being "stubborn" is exactly what the giants were expected to do over the past week or so, and the market has given varying feedback.

Under this expected "stubbornness," Capex is naturally higher than market expectations, and even higher than mine (my expectation was lower than the consensus). However, I have discussed these situations in offline exchanges: being "stubborn" means they will definitely provide very high figures to demonstrate both the seriousness of corporate governance and the firmness of strategic planning. However, physically, the final number that actually lands will surely be something else.

It's simple: it appears the market now has "zero tolerance" for the fact that "capital expenditure exceeds revenue growth," even for a company as strong as Google.

Perhaps the negative feedback has truly begun; in fact, it has arrived even earlier than the end of the second quarter, which was my previous expectation.